Property Investment Glossary

If you’re a newcomer to the world of property investment, you may find some of the jargon a little confusing. The following glossary of terms that are commonly used in relation to property investment or property purchasing may be helpful as you navigate your way through the process.

AAPR - This stands for the Average Annual Percentage Rate. It's a term use to describe the "true rate" of a loan. Mortgage Specilists use the AAPR when ranking loans in the Toolbox software. Mortgage Specilists use it to work out the real cost of a loan, because it takes into account honeymoon rates, ongoing fees, introductory offers and discharge fees as well as the advertised interest rate. The AAPR calculation is based on the actual loan amount and how much is charged for it over a 7 year period. The AAPR doesn't include government fees, exit or early repayment fees and service fees like redraw and internet usage charges.

Amortisation period -

Also known as the loan term. It’s the agreed length of time that a borrower has to repay a loan. It’s set during the application and approval process.

Appraised value - The estimated value of a property being used as security for a loan.

Basic Variable – a variable home loan at a lower rate and with fewer features than a standard variable home loan.

Break Costs – fees that are sometimes incurred when a loan is paid off early.

Bridging Finance – a short-term loan used to bridge the gap between buying a new property and selling an existing one. For example, taking out a temporary loan to settle a purchase that becomes due before the date that the longer-term finance becomes available. People who need to sell their property before they can purchase another one frequently seek bridging finance, and when their property is still on the market when settlement of the new property falls due.

Cross - securitisation/Cross-collateralisation – when the financial institution uses your property (whether owner-occupied or investment) as security for other property you purchase.

Capped loan - A loan where the interest rate cannot exceed a set level for a period of time but, unlike fixed rate loans, can fall.

Caveat - A caveat lodged upon a land or property title indicates that a party, that is not the owner, claims some right over or interest in the property.

Certificate of Title - A record of all current information relevant to a particular property or piece of land, including:

*Current ownership details.

*Any registered encumbrances or caveats.

*Lot or plan details.

A lender usually holds this document as security. Once the loan is fully repaid, the Certificate of Title is returned to the borrower.

Credit – Borrowed money or other finance to be paid back under an arrangement with a lender.

Default – Failure to abide by the terms of a mortgage or loan agreement - such as not making loan minimum required repayments. Defaulting on a loan may result in financial penalties and, in extreme cases, the mortgage holder taking legal action to repossess the mortgaged property.

Deposit – An amount paid by the buyer at the time of exchanging the contract for sale. It acts as a commitment to buy. Normally a minimum of 5-20% of the total purchase price is required.

Deposit bond – A guarantee from a financial institution that a deposit will be paid to a seller. It’s useful for buyers with savings in a term deposit because it can be offered at the time of exchange – instead of a cash deposit. Which means the buyer doesn’t have to break the term deposit and lose any interest accrued. The buyer must pay the full purchase price of the property, including the amount of the deposit, at settlement. In the event that buyer does not settle on the property the seller will be paid the deposit amount by the financial institution.

Discharge of Mortgage – A document signed by the lender and given to the borrower when a mortgage loan has been repaid in full.

Drawdown of Funds – to withdraw funds from a designated loan account, common in house and land purchases with a construction loan where building progress payments are drawn down progressively according to construction expenditure.

To access available loan funds. Draw down usually refers to a construction loan, or a line of credit. That is a loan where the limit is set, but the amount is not accessed all at once. The borrower draws down or uses the funds as required, up to the set limit.

Equity – the difference between your mortgage and your property’s value. If your home is worth $400,000 and you owe $150,000, then you have equity of $250,000. The amount of a property actually “owned” by the owner. It’s the current value of a property less the amount still owed on its mortgage. Equity usually increases as the principal of the mortgage is paid off. Market values and improvements to the property can also affect equity.

Establishment fees – Fees charged by a lender to cover the cost of setting up a loan.

Exit or early repayment fees – Penalties charged by some lenders when a loan is paid off before the end of its term.

First Home Owners Grant – A grant from the Federal and State Governments. It was introduced as compensation for the increased cost of housing after implementation of the Goods and Services Tax (GST) on 1 July 2000. It’s only for buyers that have not previously bought property in Australia.

Fixed Rate – An interest rate that applies to a loan for a set term. Both the interest rate and loan repayments are fixed for the agreed term, regardless of any interest rate variations in the home loan market. The agreed term is usually anywhere between 1 and 7 years.

Home loan – The funds borrowed to purchase a property. The property acts as security for repayment of the loan. The lender holds the title or deed to the property. It’s also known as a mortgage.

Interest-only – A loan where only the interest is paid for an agreed term, usually 1 to 5 years. The principal is then repaid over the remaining term of the loan by the conversion of repayments to principal and interest.

Introductory loan – A loan offered to new borrowers at a reduced rate for an introductory period - usually 6 to 12 months. It’s also called a discounted or honeymoon rate.

LMI (lender's mortgage insurance) – Insurance which covers the lender if a borrower defaults on a loan and the sale of the property doesn’t cover the outstanding debt. It’s usually required for the loans the lender considers more risky. For example, when the amount borrowed is over 80% of the property value. Only the lender is covered by this insurance. It offers no protection to the borrower.

LOC (line of credit) – a facility available from financial institutions that gives you a credit limit that you can draw down at any time. It’s similar to a credit card, except you don’t have to make set repayments of the principal.

Low-doc Loan – relatively new, these are loans that don’t require as much documentation to set up the loan. They are popular with self-employed people and those who have not yet established a credit rating.

LVR (loan-to-value) ratio – Abbreviation for the term Loan to Value ratio. It is the percentage of the loan amount compared to the value of that property. So if a house is worth $160,000, and the mortgage is $100,000, then the LVR is 62.50%. Most lenders require a borrower to take out Lender's Mortgage Insurance if the LVR is 80% or more.

To calculate it, divide the loan amount by the value of the property then multiply by 100 to get a percentage. Banks and financial institutions use this as a measure of whether you can afford the loan.

Mortgage offset account – his insurance covers loan repayments should a borrower become sick, injured or redundant and unable to work. It is also called income protection insurance. This insurance covers the borrower not the lender.

Mortgage Protection Insurance – A savings account linked to a home loan. The interest earned by the money in the savings account offsets - or reduces - the interest due on the home loan. A 100% offset is where the interest rates earned and paid are the same. A partial offset account is where the interest earned on the offset account is only a portion of the rate paid on the home loan.

Mortgage registration fee – A State Government charge for the registration of a loan. Because the property acts as security for a home loan, the government requires a home loan to be registered so that all claims on a property can be checked by any future buyers of that property.

Portability – Allows a different property to be substituted as security for an existing loan. Useful if you are buying a new home but don’t want to set up a new mortgage.

Principal and Interest (P&I) – the amount borrowed or still to be repaid, plus the interest on the mortgage. The principal is part of the repayment that reduces the balance of the mortgage.

Refinance – to obtain new finance for something on different terms, usually involving the paying off of an existing loan by means of a new (and often cheaper) loan.

Reverse Mortgage – designed for seniors who are asset-rich (usually with their PPOR) but cash-poor. The facility allows them to access the equity in their homes without having to sell it. Most often the loan is not paid out until the borrower dies, moves into a nursing home or relocates.

Security – An asset that a borrower gives a lender the rights to - so the lender can be confident of getting the money back, one way or another if the debt is not re-payed as per the loan agreement.

Serviceability – whether you can manage your mortgage payments, based on your income and expenses.

Stamp duty – A State Government tax based on the purchase price of the property. It’s also payable on mortgages in some states. Each state and territory has different rules and calculations. To estimate the amount of stamp duty you may have to pay, use our stamp duty calculator.

Uniform Consumer Credit Code (UCCC) – This is the legal framework that governs the relationship between borrowers and lenders. It requires all credit providers such as banks, building societies, credit unions, finance companies and businesses, to:

*Explain the borrowers rights and obligations

*Disclose all relevant information about a loan in a written contract - including interest rates, fees, and commissions.

Gearing is the process of borrowing money for the purpose of buying an investment property. Given the practical costs of owning a home, this is a process that generally requires a high, stable income. This differs from the regular purchase of a home. Most people buy a home with the intention of living in it, however investment properties are commonly purchased as secondary property. In most cases, investors are searching for tenants to help offset the costs of home ownership.

• Is designed to make a profit;

• Involves borrowing money to purchase a property;

• Differs from purchasing a home to occupy or use it;

• Makes a rental income for the owner;

• Requires a high income to maintain ongoing costs.

Positive Cash Flow – If your monthly rent is more than monthly expenses (including things like taxes, mortgages, repairs and maintenance) you have a cash flow positive property.

Positive Gearing – Positive Gearing is when the rental income on an investment property exceeds the cost of maintaining it, thus generating more income than losses. This occurs if a property is purchased and used to make a short-term profit through rent, usually at times when interest rates are low, and rental rates are high. The rent collected exceeds the cost of repayments, maintenance and interest, and the owner gains an additional income stream.

Positive gearing is primarily practiced in areas that are experiencing substantial industry and employment growth, particularly in rural areas. This surge increases demand for rental properties, which inturn allows owners to charge higher rents, and to make larger profits from the geared property. Income on a positively geared property is taxed, so people who own positively geared homes should be prepared to maintain them well, and sell while the price of their property is still high, lest they make a loss.

The Advantages of Positive Gearing

• Faster Profit- The gains from rent are immediate. Investors gain a new income stream and a short-term payoff;

• Stable Income- The property pays for itself, letting the investor maintain the property without relying too heavily on an alternate source of income;

• Builds upon itself- The extra income can help aid an investor’s atractiveness to lenders, allowing investors to build up their investment portfolio.

Negatively Geared – Negative Gearing is when a property runs at a loss for the owner, with the costs of maintenance exceeding the rental income. These kinds of investments are used to make long-term capital gains profit. The property is bought with the expectation that its value will grow over time, thus outweighing any short term financial losses.

Negative gearing creates a taxable loss, which investors offset against their primary income as a tax saving. The plan is to use your ordinary income to pay off the shortterm costs of the home, and then go on to profit off the sale of the home when its price has increased

The Advantages of Negative Gearing

• Greater Long-term Payoff- The profits earned from selling a property that has grown over time far exceed the long-term costs;

• Low Interest Rates- Interest rates in Australia are currently low. This makes negative gearing a popular alternative for investors;

• Potential for Development- Because of the long-term nature of negative gearing, investors can spend money on developing the property and increasing its market value over time.

Aspect – a compass direction e.g. a northerly aspect or westerly aspect. Cash Rate/Bank Rate – the cash rate is the rate at which the Reserve Bank of Australia sets interest rates. The bank rate is the interest rate banks offer and is above the cash rate to allow for a profit margin. Certified Copy – a true copy of an original document that has been authorised in writing by a Justice of the Peace, Commissioner for Declarations or Notary Public. Commission – the fee payable to the real estate agent for the work performed during the sale (or property management) of the property. The fee is paid by the person who authorised the agent to act on their behalf (usually the seller – or landlord, in the case of property management) and is payable upon settlement of the property (or during the course of the property management period). Conditions of Sale – the conditions under which a purchaser takes property sold to him. Where real property is the subject of sale the conditions contain provisions as to title to be accepted by the purchaser and how it is to be proved and the amount of deposit. When a sale is concluded, the purchaser signs a memorandum endorsed on the conditions, the whole becoming the contract of sale. Conditions of sale are frequently attached to goods specifying what warranties attach or do not attach and generally, the purchaser will be deemed to have notice of such conditions and they will affect the sale accordingly. Contract of Sale – an agreement relating to the sale of property which contains terms and conditions of sale. All contracts must be in writing. Cooling-off Period – a period of time given to the purchaser to legally withdraw from buying a property. The length of time varies in each of the states and territories. Covenant – is a promise executed under a seal whereby one party promises to another that something has, or will be, done. Covenants can be positive in nature, such as an undertaking by a landlord to perform certain structural alterations to make leased premises suitable for the tenant. Deposit – money paid as evidence of good faith for the future performance of a real estate transaction. It is normally held by a third party, usually the agent, in a Trust Account or by the developer’s solicitor in a Trust Account. If the purchase is completed, it will be paid towards the purchase price of the property (or in the case of property management, a holding rental deposit). Due Diligence – ensuring that sufficient analysis has been conducted before recommending an investment to a client. Easement – right to use the land of another. The most common easements are Right of Way. For example, where a property owner grants a Right to an adjoining owner for that owner to use part of the land to gain access to the adjoining owner’s land. Encumbrance – an interest or right in property, which usually diminishes the value of the land but does not prevent the transfer of ownership. Any impediment to the use of the land including such things as easements, mortgages, caveats, notices of intention to resume, or leases, which are registered on the title are encumbrances. Established home – a home that has been lived in previously. Fittings – items that can be removed from a property. Fixtures – items affixed to the structures of the land, usually in such a manner that they cannot be removed without damaging the property. The agent must list all fixtures to be included on the contract. Freehold or Fee Simple – highest form of ownership. An owner can use the land in any way desired, subject to usual zonings and other government controls. Group Title – similar to freehold except that title also includes common property owned jointly. This must involve a body corporate. Each lot has its own certificate of title and a registered number of entitlements. Entitlements include voting rights and contribution of levies to the body corporate. These may not always be equal. The body corporate owns roads, common areas, facilities and equipment supplied. Investment Property – land or a building, (or part of a building), held to earn rental income or for capital appreciation, or both. An investment property generates cash flow largely independently of other assets held, and this is the characteristic that distinguishes investment property from owner-occupied property. Investor – a person who invests money prudently and productively over the longer term with the investment objectives being achievement of a reasonable return and capital growth (appreciation) to preserve purchasing power. Also the opposite of a speculator, who will sacrifice safety of principal, for the possibility of larger gains. Joint Tenant – two or more ways in which two persons may own property together. The rule of survivorship applies. When a joint tenant dies then the surviving joint tenant automatically gains entitlement to the deceased person’s share of the property. Joint tenants have equal share. Market Value – as defined by the courts, the highest price estimated in terms of money which a property will bring if exposed for sale in the open market allowing a reasonable time to find a purchaser who buys with knowledge of all the uses to which it is adapted and for which it is capable of being used and assumes a willing buyer and willing seller. Off the Plan (also known as Off-Market or Off-Plan) – when you buy off the plan, you are buying a property before it is built, having only seen the plans. This is commonly used for apartments or units under construction or about to be built. POA – price on application. You may see this in a real estate advertisement. Portfolio (as in property portfolio) – the number and type of investment properties you own. Strata Title – system of land title based on the horizontal sub-division of air space whereby all the owners combined own the land, but have absolute right to sell/transfer their strata-titled property to a new owner. The most common form of strata title is a home unit. Torrens Title – most common and simplest form of an individual certificate of title to a property. Torrens System – this is the name given to a system whereby title to land is evidenced by one document issued by a Government Department. Trust Account – bank account relating to monies received or held by an agent or a developer for or on behalf of another person. Monies held in trust are protected at law. Vendor/Seller – person/entity that offers a property for sale.

FIRB (Foreign Investment Review Board) – examines proposals by foreign people and companies to invest in Australia and advises the Treasurer on those subject to the Foreign Acquisitions and Takeovers Act 1975 and Australia’s foreign investment policy. FIRB Purchaser – a foreign person purchaser who requires FIRB approval in order to be able to legally purchase a property. Foreign Person – the term Foreign Person means: • A natural person not ordinarily resident in Australia; • A corporation in which a natural person not ordinarily resident in Australia or a foreign corporation holds a controlling interest; • A corporation in which 2 or more persons, each of whom is either a natural person not ordinarily resident in Australia or a foreign corporation, hold an aggregate controlling interest; • The trustee of a trust estate in which a natural person not ordinarily resident in Australia or a foreign corporation holds a substantial interest; or • The trustee of a trust estate in which 2 or more persons, each of whom is either a natural person not ordinarily resident in Australia or a foreign corporation, hold an aggregate substantial interest.

Building Approval – the number of dwellings approved to be constructed in a given month, quarter or year. Final Inspection Report – a certification issued by a local council or building inspector that building works for a home are complete and the home is ready to be lived in. Right of Way – A person may have a right to cross your property to gain access to his/her own property or there may be a public pathway across the land. Square – an old imperial unit of area measurement. 1 square = 10 feet x 10 feet in area, which in metric measure is equivalent to 9.29m2. Strata Title – system of land title based on the horizontal sub-division of air space whereby all the owners combined own the land, but have absolute right to sell / transfer their strata-titled property to a new owner. The most common form of strata title is a home unit. Subdivision – a parcel of land divided into individual lots. Urban Renewal – the process of rehabilitating urban (city) areas, by demolishing, remodelling or repairing existing structures and buildings, public buildings, parks, roadways and individual areas on cleared sites in accordance with a more or less comprehensive plan.

Stamp Duty (also called Transfer Duty) – a state government tax on the transfer of property calculated on the value of the property. Certificate of Title – the document of title to land held under the Torrens Title system. It shows who owns the land, and whether it is subject to mortgage, lease, easement or any other dealing, which may adversely affect a potential buyer. Conveyancing – the process that legally transfers property ownership from one entity to another. Group Title – similar to freehold except that title also includes common property owned jointly. This must involve a body corporate. Each lot has its own certificate of title and a registered number of entitlements. Entitlements include voting rights and contribution of levies to the body corporate. These may not always be equal. The body corporate owns roads, common areas, facilities and equipment supplied. Joint Tenants – each owner has equal shares and rights in the property. RP (Registered Plan) – plan number in the Titles Office. The RP number is the sub-divisional plan, which includes the dimensions and details of the particular parcel of land. RPD (Real Property Description) – method of describing a particular parcel of land. For example, Lot 3 on RP 546789 identifies the plan number and then the particular lot number. A plan search at the Titles Office would give an agent or a potential buyer a copy of the sub-divisional plan and dimensions of each lot on the plan. Settlement – occurs when the buyer becomes entitled to possession of the property. A formal settlement occurs when the owners hand to the buyer the executed transfer documents and the Certificate of Title in exchange for payment of the balance of purchase monies. Tenants in Common – two or more buyers own a property with unequal shares and rights. Title Deed– document showing ownership of property. Also records details of any mortgage, encumbrance and area. Transfer – the document used to transfer the interests of a registered proprietor to a purchaser by means of lodgement at, and acceptance by the titles office.

Appraisals/Valuations – a written report of the estimated value of a property, usually prepared by a valuer.

Appreciation – an increase in value.

Basis Point – a measurement of fluctuation of an investment, equal to 1/100 of one percent.

Capital Growth (Capital Gain) – appreciation in the capital or market value of an investment. The amount by which your investment property has increased relative to what you paid for it. For example, if you bought a property for $400,000 and it’s now worth $500,000, you’ve made a capital gain of $100,000 (the difference between the purchase price and selling price in the sale of an asset (the actual profit made).

Consumer Price Index (CPI) – an index measuring the prices at various times of a selected group of goods and services which typify those bought by ordinary Australian households. It allows comparisons of the relative cost of living over time, and is used as a measure of inflation.

Diversification – the spreading of investment funds among classes of securities and localities in order to distribute and control risk. This is a fundamental law of investing, meaning simply: Don’t put all your eggs in one basket.

Economic Clock – a model (represented by the face of a clock) for depicting the normal sequence of events for share and property market cycles. After interest rates fall, the share market rises, followed by commodities, inflation and property. Interest rates then rise to curb inflation and the cycle goes into decline, before repeating over again. Note that not all cities / states are at the same place on the clock at the same time.

Lower Quartile – the price point below which 25 per cent of sales were recorded. If there were 100 sales in a suburb, the 25th lowest price would be the lower quartile price.

Median Price – the median house price is the middle price of all sales recorded in a particular suburb, postcode, city or state. If there were 100 sales in a particular suburb, in ascending order, the median would be number 50 on the list. It’s commonly assumed that the median price is the same as the average price, but that’s not the case. To calculate the average, you would add up the 100 sales and divide the total by 100 (the number of sales) and the number could be quite different to the medium.

Property Cycle – property values usually follow a cycle of growth, a slowdown, a bust and an upturn. History shows this occurs every seven to ten years.

Supply and demand – the number of properties on the market at any given time determines the supply-and-demand equation. If there are lots of properties on the market, it’s a buyers’ market. If there are few properties on the market or those that come on to the market sell quickly, then it’s a sellers’ market.

Upper quartile – the price point below which 75 per cent of sales were recorded. If there were 100 sales in a suburb, the 25th highest price would be the upper-quartile price.

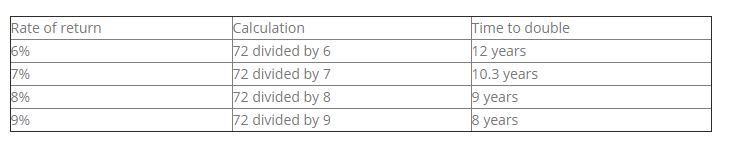

Rule of 72 – a convenient technique to estimate compound interest rates derived from the fact that a 7.2 per cent return rate per year is the rate that will double the value of an investment in ten years. Hence, years to double an investment with a given annual rate of return can be estimated by dividing the rate of return into 72. See chart below:

Similarly, the rate of return needed to double the value of an investment in a given number of years can be estimated by dividing the number of years to double into 72. For example, if an investor plans to hold an asset for 9 years, it will need a return rate of 8 per cent per annum (72 divided by 9).

Similarly, the rate of return needed to double the value of an investment in a given number of years can be estimated by dividing the number of years to double into 72. For example, if an investor plans to hold an asset for 9 years, it will need a return rate of 8 per cent per annum (72 divided by 9).

Body Corporate – an administrative body made up of all the owners within a group of units or apartments of a strata building complex. The owners elect a committee, which handles administration and upkeep of the building and common areas. Also known as owners’ corporation. Common Property – 1. Land or a tract of land considered as the property of the public in which all persons enjoy equal rights. A property not owned by individuals but by groups. 2. In a home (villa) unit or flat development that part of the property owned and used in common by all the unit or flat owners or occupiers and which is maintained by the Body Corporate. Landlord – owner of leased/rented property. Leasehold – owner of property allows another person to have possession of property in return for rent. Term can vary from 1 day to 99 years. The majority of residential tenancies are either 6 or 12 months. Commercial leases are generally under 10 years and most often for a 3-year period. Lessee – tenant who has the right to use or occupy a property under lease. Lessor – landlord who holds title and conveys the right to use and occupy a property under a lease agreement. Property Management – a division of a real estate office composed of leasing space, collection of rents, selection of tenants and generally the overall maintaining and managing of real estate properties for clients. Rental Yields (and calculations) – the return on an investment as a percentage of the amount invested. Gross rental yield can be calculated by multiplying the weekly rent by 52 (weeks in a year), then dividing by the value of the property and multiplying this figure by 100 to get the percentage. For example if a property is rented for $400 per week, and the purchase price was $450,000, then the yield is (($400*52)/$450,000)*100 = 4.62 per cent. Vacancy Rates – a measure of how many dwellings are available for rent over a specified time period. A low vacancy rate means there are not very many dwellings available for rent, while a high vacancy rate means there is ample supply of rental properties. Vendor – the seller. Yield – the return by an investor on an investment, shown as a percentage of the amount invested.

Income Protection Insurance – this insurance cover is a cash flow protection method to ensure you can fund your outgoings of daily life and the possible shortfalls of your property portfolio. Landlords Protection Insurance – insurance designed to protect the Landlord. Common features of a landlord insurance policy include: • Malicious or intentional damage to the property by the tenant or their guests (above that which may be covered by Rental Bond monies); • Theft by the tenant or their guests; • Loss of rent if the tenant defaults on their payments; • Liability, including for a claim against you by the tenant, and • Legal expenses incurred in taking action against a tenant. Lenders Mortgage Insurance (LMI) – usually required by lenders when you’re borrowing more than 80 per cent of the property’s value. It provides insurance to the lender in case the borrower defaults on the loan. Life, Trauma and TPD Insurance – this cover is about insurance covering accidents/circumstances which cause death (life cover), a serious health issue like cancer and illnesses that impede your ability to work for a certain time (trauma cover) or a serious impairment that would take away your ability to ever work again (TPD cover).

ATO – abbreviation for Australian Taxation Office. Capital Gains Tax – a tax payable when/if you sell a property. It’s a tax on the increase in the capital value of investments. Capital gains tax is indexed so that nominal increases in value due to inflation are not taxed as well. The taxation regime also allows capital losses to be offset against other taxation liabilities (e.g. income tax) in certain circumstances. This is the tax you pay when you sell an investment property if you’ve made a profit. Depreciation – as buildings get older and items within it wear out, they depreciate in value. The Australian Taxation Office allows property investors to claim deductions related to the building (Capital Works) and Plant and equipment items in it. The owner of an income-producing investment property can claim depreciation; this has the effect of reducing their taxable income, meaning they pay less tax. Capital Works – the capital works allowance is a deduction available for the structural element of a building including fixed irremovable assets; this is commonly referred to as the building write off. Only some properties will qualify for this allowance. For residential buildings constructed after 16 September 1987 your accountant can claim 2.5 per cent of its historical construction cost. Plant and Equipment – refers to removable items in the investment property like carpet, hot water systems, blinds, light fittings and many other items. PPOR or PPR – principal place of residence. Generally, a residence is your PPR if you live in it (with your personal belongings) on a daily basis. Other factors may be used to determine whether a residence is your PPR, such as: • Where your family lives; • The extent of time you live in the residence; • The address you have your mail delivered to; • Whether utilities (e.g. electricity, gas and telephone) are connected to the dwelling and the account(s) are in your name; and • If the address of the residence is recorded against your name on electoral rolls. Tax File Number (TFN) – a number allocated to taxpayers by the Australian Taxation Office. The TFN is used by the Australian Taxation Office to match income and taxation details.

Useful Links - Government & Research Sites

Australian Bureau of Statistics – http://www.abs.gov.au Australian Taxation Office – https://www.ato.gov.au CoreLogic (previously known as RP Data) – http://www.corelogic.com.au Residex – http://www.residex.com.au Real Estate Institute of Australia – http://reia.asn.au New South Wales – Fair Trading – http://www.fairtrading.nsw.gov.au National Rental Affordability Scheme – https://www.dss.gov.au/our-responsibilities/housing-support/programmes-services/national-rental-affordability-scheme BIS Shrapnel – http://www.bis.com.au/home.html Due diligence checklist – for residential property buyers – http://www.consumer.vic.gov.au/duediligencechecklist